Strategic planning requires a clear understanding of the competitive landscape. Without visibility into market dynamics, organizations make decisions based on assumptions rather than data. Michael Porter’s Five Forces framework provides a structured method to evaluate industry profitability and intensity. This guide explores how this model functions across three distinct sectors: Technology, Retail, and Healthcare.

Each industry operates under unique regulatory, economic, and behavioral pressures. What drives competition in software differs vastly from what drives it in pharmaceuticals or brick-and-mortar stores. By dissecting these forces, decision-makers can identify vulnerabilities and opportunities. The following sections break down the mechanics of the analysis and demonstrate its practical application.

🧠 Understanding the Framework Defined

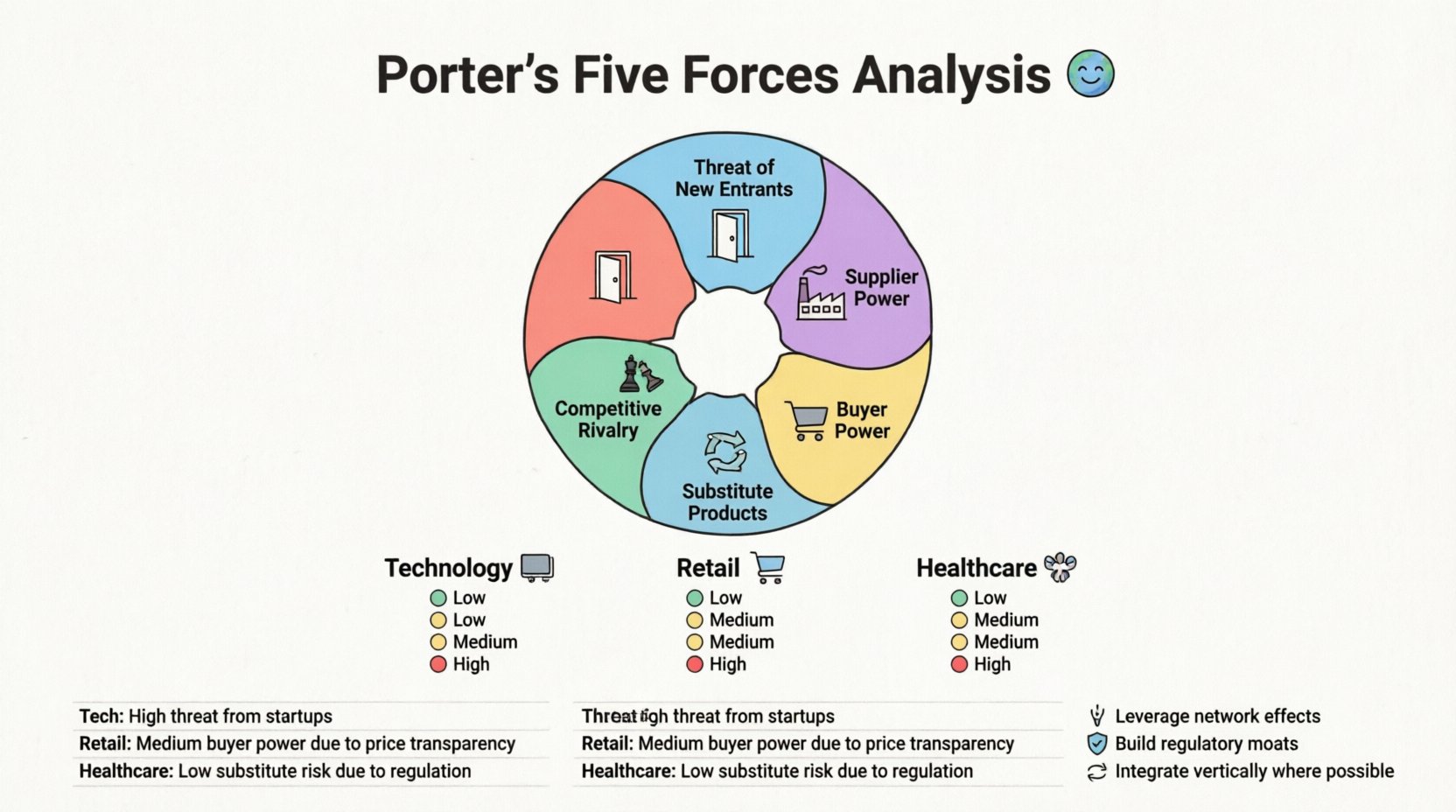

The model assesses five specific forces that shape competition. These forces determine the long-term profit potential of an industry. When these forces are intense, profitability tends to be low. When they are weak, profitability is generally higher. The five components include:

- Threat of New Entrants: The ease with which competitors can enter the market.

- Bargaining Power of Suppliers: The ability of suppliers to drive up prices.

- Bargaining Power of Buyers: The ability of customers to drive down prices.

- Threat of Substitute Products: The availability of alternative solutions to the core offering.

- Rivalry Among Competitors: The intensity of competition between existing firms.

Understanding the baseline intensity of each force is the first step. In a healthy market, these forces are balanced. In a turbulent market, one or more forces may dominate the strategic landscape. Organizations must evaluate each force individually before synthesizing the findings into a broader strategy.

💻 Technology Sector Analysis

The technology industry is characterized by rapid innovation and high capital requirements for research and development. Market dynamics shift frequently due to software updates and hardware advancements. Applying the Five Forces here requires a focus on intellectual property and network effects.

1. Threat of New Entrants

In the tech sector, barriers to entry vary significantly depending on the sub-sector.

- Software as a Service (SaaS): Barriers are relatively low. Cloud infrastructure reduces the cost of deployment. However, customer acquisition costs are high, and switching costs for enterprise clients can be significant.

- Hardware Manufacturing: Barriers are high. Supply chain complexity, patent litigation, and capital expenditure create substantial hurdles for new players.

- Platform Ecosystems: Network effects create a moat. A new social platform has little value if no one else is on it. This discourages entry despite low technical barriers.

2. Bargaining Power of Suppliers

Suppliers in tech often include specialized chip manufacturers, cloud providers, or talent pools.

- Specialized Hardware: If a company relies on a single source for a critical component, supplier power is high.

- Cloud Infrastructure: A few major providers dominate the market. Migration costs can lock companies into specific ecosystems, giving the provider leverage.

- Talent: Skilled engineers are a scarce resource. This gives skilled labor high bargaining power regarding compensation.

3. Bargaining Power of Buyers

Buyers in technology range from individual consumers to large enterprise organizations.

- Enterprise Clients: Large organizations have significant negotiating power. They demand customization, security compliance, and volume discounts.

- Individual Consumers: Switching costs are often low. A user can move from one messaging app to another with little friction. This increases buyer power.

4. Threat of Substitute Products

Substitution is a constant threat in tech due to the speed of innovation.

- Digital Transformation: Traditional fax machines were replaced by email and VoIP. Companies that fail to adapt face obsolescence.

- Alternative Workflows: If a new tool solves a problem more efficiently, adoption shifts quickly. The definition of “product” often expands to include services.

5. Rivalry Among Competitors

Competition is fierce and often driven by pricing wars or feature parity.

- Price Wars: In commoditized segments, price becomes the primary differentiator.

- Innovation Race: Companies race to release features first. Being the first to market does not guarantee longevity if competitors catch up quickly.

🛒 Retail Sector Analysis

The retail industry encompasses both physical locations and digital storefronts. Margins are often thin, making efficiency critical. The rise of e-commerce has shifted power dynamics significantly over the last decade.

1. Threat of New Entrants

Digital retail has lowered barriers to entry, while physical retail remains challenging.

- E-commerce: Setting up a store is easier than ever. Third-party logistics allow small brands to reach global audiences.

- Physical Locations: Rent, staffing, and local regulations remain significant barriers. Established locations have a legacy advantage.

- Brand Recognition: New entrants must spend heavily on marketing to gain trust against established retailers.

2. Bargaining Power of Suppliers

Retailers rely on a vast network of manufacturers and distributors.

- Commoditized Goods: For generic items, supplier power is low. Many factories can produce the same product.

- Exclusive Brands: If a retailer stocks a popular brand exclusively, that supplier gains leverage regarding pricing and terms.

- Private Label: Retailers developing their own brands reduce dependence on external suppliers, shifting power back to the retailer.

3. Bargaining Power of Buyers

Buyers in retail have immense power, particularly online.

- Price Comparison: Consumers can compare prices across dozens of sites in seconds. This transparency forces competitive pricing.

- Switching Costs: Low. A customer can leave a loyalty program or stop visiting a store with no penalty.

- Convenience: Buyers value speed and ease of delivery. Retailers must invest in logistics to satisfy this demand.

4. Threat of Substitute Products

Substitution in retail often comes from changing consumer habits.

- Online vs. Offline: Physical stores face substitution from online marketplaces.

- Direct-to-Consumer: Manufacturers are bypassing retailers to sell directly to customers. This cuts out the middleman.

5. Rivalry Among Competitors

Competition is intense, driven by location and price.

- Location Saturation: In urban centers, multiple retailers may operate on the same block.

- Promotional Cycles: Frequent sales events train consumers to wait for discounts, eroding margins.

🏥 Healthcare Sector Analysis

Healthcare is highly regulated and driven by necessity rather than discretionary spending. This creates a unique set of competitive forces compared to consumer goods.

1. Threat of New Entrants

Barriers to entry are exceptionally high due to regulation and capital.

- Licensing: Medical devices and pharmaceuticals require rigorous testing and approval processes.

- Reimbursement: Navigating insurance billing codes is complex. New entrants face steep learning curves.

- Trust: Patients and providers prefer established institutions with proven track records.

2. Bargaining Power of Suppliers

Suppliers include pharmaceutical companies, equipment manufacturers, and insurance providers.

- Patent Protection: Pharmaceutical suppliers hold significant power due to exclusive rights to specific drugs.

- Medical Equipment: Specialized machines often come from a single vendor. Maintenance contracts can lock providers in.

- Insurance Payers: Large insurance companies dictate reimbursement rates, acting as powerful gatekeepers.

3. Bargaining Power of Buyers

Buyers in healthcare are complex. They are often patients, but payers are employers or the government.

- Patients: In emergencies, price sensitivity is low. Patients require care regardless of cost.

- Government: In many systems, the government is the primary payer. This centralizes bargaining power and dictates pricing structures.

- Employers: Large employers negotiate group rates for employee health coverage, reducing the provider’s pricing power.

4. Threat of Substitute Products

Substitution is limited by medical necessity.

- Treatment Alternatives: While different therapies exist, few are perfect substitutes for life-saving procedures.

- Telemedicine: This has emerged as a substitute for routine check-ups, changing the delivery model significantly.

5. Rivalry Among Competitors

Competition focuses on outcomes, reputation, and network access.

- Hospital Networks: Mergers create large networks that negotiate better with insurers.

- Quality Metrics: Hospitals compete based on patient outcomes and safety records.

📊 Comparative Overview of Industry Forces

The table below summarizes the intensity of each force across the three sectors. High intensity indicates a challenge to profitability. Low intensity suggests a more stable environment.

| Force | Technology | Retail | Healthcare |

|---|---|---|---|

| Threat of New Entrants | Mixed (Low for Hardware, High for SaaS) | Medium (Low for E-com, High for Physical) | Low (High Regulatory Barriers) |

| Bargaining Power of Suppliers | Medium to High (Talent & Chips) | Low to Medium (Commoditized Goods) | High (Pharma & Insurance) |

| Bargaining Power of Buyers | High (Low Switching Costs) | Very High (Price Transparency) | Low to Medium (Payers Drive Cost) |

| Threat of Substitutes | High (Rapid Innovation) | High (Online vs Offline) | Low (Medical Necessity) |

| Rivalry Among Competitors | High (Innovation Race) | Very High (Price Wars) | Medium (Differentiation by Quality) |

📝 Strategic Implementation Steps

Conducting this analysis is not a one-time event. It requires a systematic approach to gather accurate data and derive actionable insights.

- Data Collection: Gather internal sales data, customer feedback, and market reports. Identify trends in pricing and volume.

- Stakeholder Interviews: Speak with sales teams, procurement officers, and product managers. Frontline staff often see competitive pressures first.

- Competitor Profiling: Document the strengths and weaknesses of key rivals. Analyze their pricing strategies and distribution channels.

- Force Scoring: Rate each force from 1 to 5 based on intensity. 1 represents weak pressure, 5 represents extreme pressure.

- Scenario Planning: Model how changes in one force might impact others. For example, how would a new supplier regulation affect costs?

This process ensures that strategies are built on a solid foundation. It moves the conversation from guesswork to evidence-based planning. Teams should review the findings annually to account for market shifts.

⚠️ Limitations and Considerations

While powerful, the framework has limitations that must be acknowledged.

- Static Snapshot: The model represents a specific point in time. Fast-moving industries may render findings obsolete quickly.

- Focus on Industry: It emphasizes external factors but may underweight internal capabilities. A strong team can overcome external pressure.

- Digital Disruption: Traditional industry boundaries are blurring. Tech companies are entering healthcare. Retailers are moving into services. Cross-industry forces must be considered.

- Complementors: The original model did not account for companies that enhance the value of a product. In modern ecosystems, partners often drive growth more than competitors.

Recognizing these boundaries allows analysts to supplement the model with other strategic tools. Combining this analysis with SWOT or PESTLE provides a more holistic view. The goal is not to predict the future with certainty, but to prepare for multiple possibilities.

🔍 Final Thoughts on Market Dynamics

Applying the Five Forces model requires discipline and objectivity. It is easy to assume a market is stable when it is actually volatile. It is equally easy to overestimate the threat of a new entrant while ignoring the power of a loyal customer base.

Success comes from recognizing the specific pressure points in your sector. In technology, innovation speed is the key metric. In retail, logistics and price transparency define the game. In healthcare, regulation and reimbursement dictate the landscape.

By continuously monitoring these forces, organizations can adjust their positioning before market conditions change. This proactive stance is the difference between reacting to disruption and shaping the future of the industry.