Understanding the structural forces that shape competition is fundamental to strategic planning. Michael Porter introduced a framework in 1979 that remains a cornerstone of business analysis today. The Porter Five Forces model provides a structured way to evaluate the intensity of competition and the profitability potential within a specific market. This guide explores the framework in depth, examining how these forces manifest differently across diverse industries.

🔍 The Framework Defined

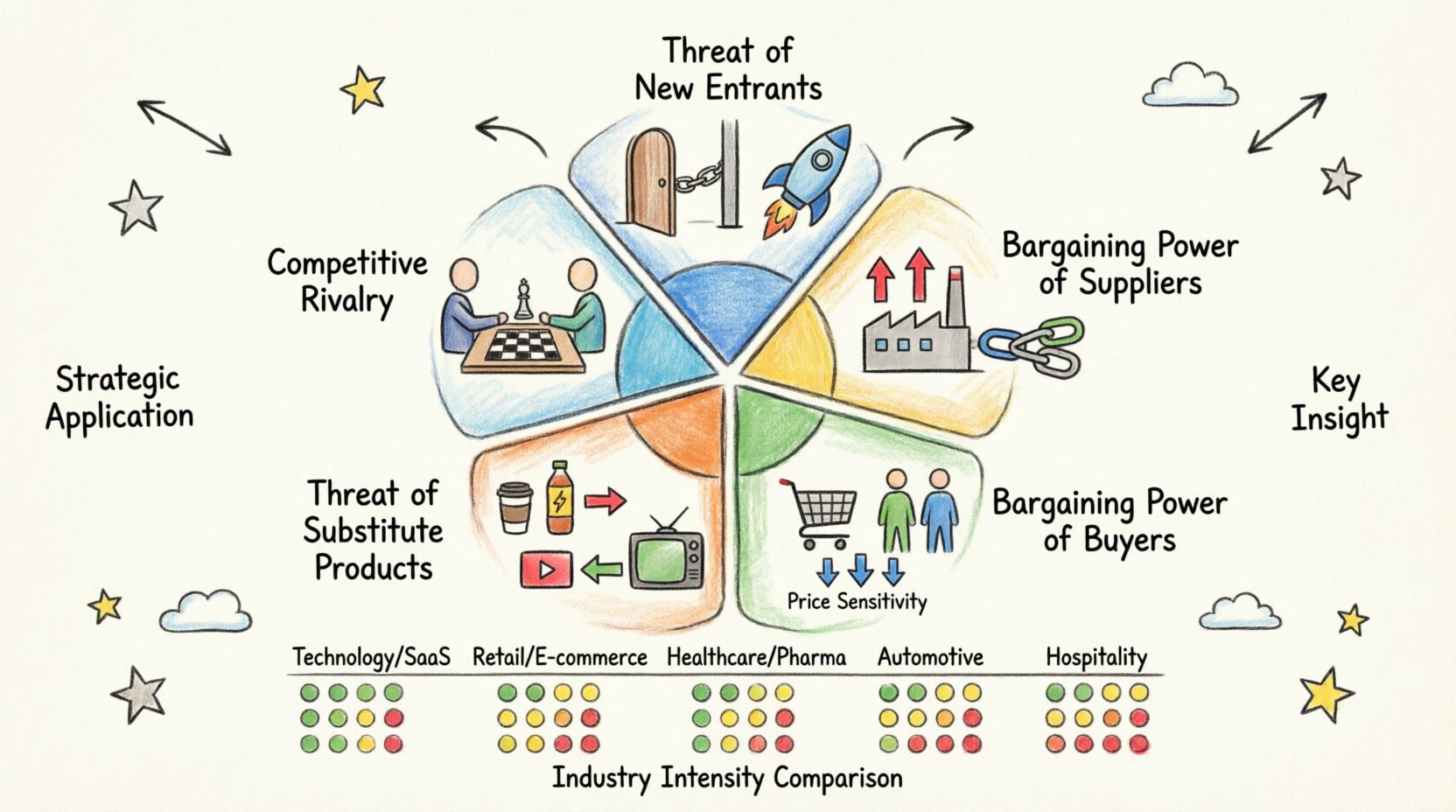

Porter identified five distinct forces that determine the competitive intensity and attractiveness of a market. These forces collectively dictate the profit potential of an industry. When these forces are strong, profitability tends to decline. When they are weak, the industry offers greater opportunities for sustained returns. The analysis requires a deep dive into the economic and structural characteristics of the sector in question.

The model moves beyond simple competitor analysis. It forces an organization to look outward at suppliers, customers, and the broader environment. This holistic view helps leaders identify where power lies and where vulnerabilities exist. Strategic decisions regarding pricing, product development, and market entry rely heavily on this understanding.

- Threat of New Entrants: How easy is it for competitors to enter the market?

- Bargaining Power of Suppliers: How much control do suppliers have over prices?

- Bargaining Power of Buyers: How much pressure can customers exert on prices?

- Threat of Substitute Products: Are there alternative solutions available?

- Competitive Rivalry: How intense is the competition among existing firms?

🚀 Force 1: Threat of New Entrants

The threat of new entrants refers to the likelihood that competitors will enter the market. High barriers to entry protect existing firms from new competition. Low barriers invite a flood of new players, driving down margins. Barriers can be structural, financial, or regulatory.

Barriers to Entry Factors:

- Capital Requirements: High initial investment acts as a deterrent. Industries like aerospace or automotive require billions in capital. A startup cannot simply build a car factory overnight.

- economies of Scale: Large incumbents produce at lower costs per unit. New entrants struggle to match these prices without significant volume.

- Regulatory Policies: Patents, licenses, and government restrictions create legal hurdles. Pharmaceutical companies rely heavily on patent protection to maintain exclusivity.

- Brand Loyalty: Established brands command trust. Breaking into a market where customers are loyal to incumbents requires significant marketing spend.

In the technology sector, barriers have shifted. While hardware requires capital, software often relies on network effects. A new social media platform faces a high hurdle because users migrate to where their friends already are. Conversely, in the food service industry, barriers are low. Opening a coffee shop requires relatively little capital, leading to high saturation and intense competition.

⚖️ Force 2: Bargaining Power of Suppliers

Suppliers can squeeze profitability by raising prices or reducing quality. This power is significant when there are few suppliers or when switching costs are high. If a supplier is a critical source of a unique input, they hold leverage over the industry.

Supplier Power Indicators:

- Supplier Concentration: If a few companies control the supply, they dictate terms. The semiconductor industry often sees this dynamic with chip manufacturers.

- Switching Costs: If changing suppliers is expensive or difficult, the current supplier holds power. Proprietary software or specialized machinery creates this lock-in.

- Threat of Forward Integration: Suppliers can enter the buyer’s industry. A steel mill might decide to manufacture cars instead of just selling steel.

- Criticality of Input: If the input is a major component of the final product, the supplier is vital. Rare earth metals are essential for electronics, giving miners significant influence.

In the airline industry, suppliers are powerful. There are only two major aircraft manufacturers, Boeing and Airbus. Airlines have little choice but to accept their pricing structures. In contrast, the retail sector faces many suppliers of generic goods. A grocery store can easily switch between food producers, reducing supplier power.

🛒 Force 3: Bargaining Power of Buyers

Buyers exert pressure to lower prices or demand higher quality. When buyers are concentrated or purchase in large volumes, they wield significant influence. They can also play competitors against each other to secure better deals.

Buyer Power Drivers:

- Concentration of Buyers: Few buyers purchasing large volumes hold power. A government contract for military equipment gives the state immense leverage over defense contractors.

- Price Sensitivity: If products are commoditized, buyers switch based on price alone. This is common in agriculture or raw materials.

- Availability of Information: Modern technology allows buyers to compare prices instantly. This transparency reduces the advantage of sellers.

- Threat of Backward Integration: Buyers can produce the product themselves. A car manufacturer might decide to build its own batteries to avoid supplier dependency.

In the business-to-business software market, enterprise clients often have high power. They negotiate multi-year contracts and demand extensive customization. However, in consumer retail, individual buyers have less power because they purchase small quantities. Yet, the aggregate demand of millions of consumers drives market trends, forcing brands to adapt quickly.

🔄 Force 4: Threat of Substitute Products

Substitutes are products from other industries that satisfy the same need. They place a ceiling on prices. If a substitute is cheaper or better, customers will switch. This force is often overlooked because it involves competitors outside the immediate industry.

Substitute Dynamics:

- Price-Performance Trade-off: If a substitute offers better value, it threatens the core product. Streaming services substituted cable television by offering lower prices and more flexibility.

- Switching Costs: If switching to a substitute is easy, the threat is high. Video conferencing tools replaced many business travel needs during recent global shifts.

- Customer Loyalty: Strong habits can protect against substitutes. People continue to drive cars despite the availability of trains, due to convenience.

The beverage industry illustrates this well. Coffee shops face competition not just from other cafes, but from tea houses, energy drinks, and home brewing equipment. In the energy sector, renewable sources act as substitutes for fossil fuels. As technology improves the efficiency of solar panels, the threat to traditional power plants increases.

⚔️ Force 5: Competitive Rivalry

This force represents the intensity of competition among existing firms. It is often the most visible aspect of industry analysis. High rivalry leads to price wars, advertising battles, and increased innovation costs.

Rivalry Intensifiers:

- Number of Competitors: Many equally balanced competitors lead to instability. If one firm lowers prices, others must follow to retain market share.

- Industry Growth Rate: In stagnant markets, firms fight for market share. In growing markets, they can grow without fighting.

- Product Differentiation: If products are identical, competition is price-based. Unique features allow for premium pricing and less direct conflict.

- Exit Barriers: If it is hard to leave the industry, firms stay and fight. High fixed costs mean companies operate at a loss rather than shut down.

The smartphone operating system market is a duopoly with high rivalry. The two main players constantly innovate to maintain dominance. In the airline industry, rivalry is fierce due to high fixed costs and low differentiation on routes. Firms compete aggressively on price, often eroding profits.

🌍 Sector Comparative Analysis

Applying the framework across different sectors reveals distinct strategic landscapes. The following comparison highlights how the forces vary in intensity depending on the industry context.

📊 Industry Force Intensity Matrix

| Sector | New Entrants | Supplier Power | Buyer Power | Substitutes | Rivalry |

|---|---|---|---|---|---|

| Technology / SaaS | Medium | Low | High | Medium | High |

| Retail / E-commerce | Low | Medium | Very High | High | Very High |

| Healthcare / Pharma | Very Low | Medium | Low (Insurance) | Medium | Low |

| Automotive Manufacturing | Low | High | Medium | Medium | High |

| Hospitality / Hotels | Medium | Low | High | Medium | Medium |

Technology Sector: High rivalry and buyer power characterize this space. Platforms compete for attention, and users can switch apps easily. However, supplier power is low as code is a common resource.

Retail Sector: Buyer power is the dominant force here. Customers demand low prices and fast delivery. Rivalry is intense as margins are thin. Substitutes are abundant in the form of direct-to-consumer brands.

Healthcare Sector: Regulatory barriers make entry very difficult. This protects existing firms. However, insurance companies act as powerful intermediaries, negotiating prices with providers. Substitutes are limited due to the critical nature of health.

Automotive Sector: Capital requirements create high barriers. Suppliers of specialized components hold power. Rivalry is high as global players fight for volume to cover fixed costs.

🛠️ Strategic Application

Conducting this analysis is not an end in itself. It informs strategic choices. Leaders use the findings to position their organizations for advantage.

- Cost Leadership: If rivalry is high and products are commodities, minimizing costs is key. Achieving scale allows for lower prices than competitors.

- Differentiation: If buyer power is high, unique features reduce price sensitivity. Brands invest in quality and service to justify premiums.

- Niche Focus: If entry barriers are low, targeting a specific segment reduces direct competition. Serving a specialized need creates a moat.

- Vertical Integration: To counter supplier power, a company might acquire a supplier. To counter buyer power, a company might acquire a distributor.

Strategic moves must be aligned with the force structure. A strategy that works in a low-rivalry industry may fail in a high-rivalry environment. Continuous monitoring is required as forces shift over time.

⚠️ Limitations & Evolution

While powerful, the framework has limitations. It is a static snapshot of a dynamic market. It assumes industry boundaries are clear, which is less true in the digital age. Platforms often blur lines between industries.

Key Considerations:

- Complementors: Porter originally focused on five forces. Some analysts add a sixth force: complementors. Products that add value when used together (e.g., hardware and software) can enhance value chains.

- Disruption: Rapid technological change can render an industry obsolete overnight. A five-force analysis might not predict a paradigm shift.

- Globalization: Supply chains are global. Local analysis might miss international competitive pressures.

Modern strategy requires combining this framework with other tools. Network effects, platform economics, and ecosystem dynamics play larger roles today. However, the core logic of understanding power dynamics remains valid.

📈 Future Outlook

The landscape of competition is evolving. Sustainability and ethical sourcing are becoming new barriers to entry. Consumers demand transparency, influencing buyer power. Regulatory shifts regarding data privacy affect technology markets significantly.

Companies must remain agile. A static analysis today may be outdated tomorrow. Regular updates to the assessment ensure strategies remain relevant. The goal is not just to survive the forces but to shape them where possible.

🏁 Final Thoughts

Strategic clarity comes from understanding the invisible structures of the market. The Porter Five Forces model offers a rigorous method to uncover these dynamics. By analyzing threats, power, and rivalry, organizations can make informed decisions.

Success depends on accurate data and honest assessment. Leaders must avoid optimism bias and acknowledge where power truly lies. Whether in high-tech or traditional manufacturing, the principles of competitive analysis provide a roadmap for sustainable growth.

Applying this framework across sectors reveals that no single strategy fits all. Context is king. The ability to adapt the analysis to specific industry nuances determines long-term viability. Continuous learning and adaptation remain essential in a changing business environment.